Credit unions are member-owned, nonprofit institutions that often offer better interest rates, lower fees, and more flexible loans, especially for members rebuilding credit. Banks, on the other hand, are profit-driven, with more branches and advanced tech but typically higher fees and lower savings returns. If you value personalized service and community focus, credit unions may suit you better. Want to discover which option fits your needs? Keep exploring to find out more.

Key Takeaways

- Credit unions are member-owned, non-profit entities offering better rates and lower fees compared to profit-driven banks.

- They benefit from tax exemptions, passing savings to members through higher interest on deposits and lower loan rates.

- Credit unions often have more flexible lending criteria, aiding members with less-than-perfect credit or unique financial needs.

- They typically charge fewer fees and participate in extensive ATM networks, reducing transaction costs for members.

- While banks may provide more branches and advanced technology, credit unions emphasize personalized, community-focused service.

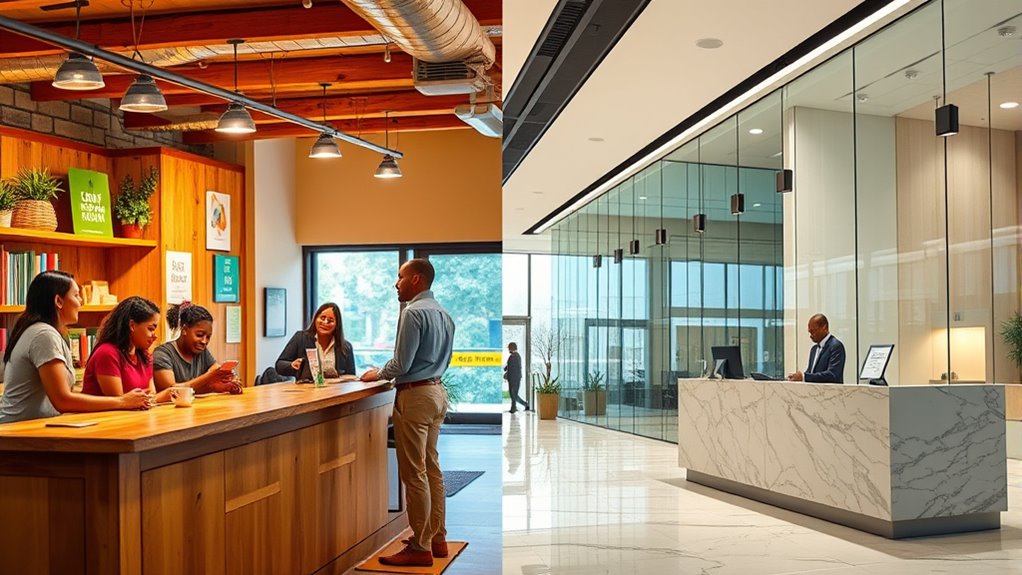

When choosing between credit unions and banks, understanding their fundamental differences can help you make better financial decisions. Credit unions are member-owned cooperatives that operate on a not-for-profit basis, meaning they prioritize serving their members rather than maximizing profits. Banks, on the other hand, are for-profit corporations owned by shareholders, with their primary goal being profit generation. This difference influences how each institution is governed: credit unions are democratically run, often with volunteer boards that reflect their local communities. Banks have no membership restrictions and are driven by corporate interests, seeking to provide value to shareholders. Usually, credit unions restrict membership by community, employment, or affiliation, while banks are accessible to anyone.

Because of their nonprofit status, credit unions benefit from a federal tax exemption, which allows them to pass savings on to members through better rates and lower fees. Banks pay federal taxes, although some may use tax structures like Subchapter S to reduce their tax burden. This distinction markedly impacts pricing and rates. Credit unions tend to offer higher interest rates on deposit accounts and certificates of deposit (CDs). For example, a 5-year CD at a credit union averages 2.66%, compared to 1.83% at banks in 2023. Money market accounts and short-term CDs also yield better returns at credit unions, helping members grow their savings more effectively. Additionally, credit unions often have more flexible lending criteria, making it easier for members with less-than-perfect credit to qualify for loans. This flexibility can be particularly beneficial for members working to rebuild credit or facing unique financial circumstances.

Fees are another advantage. Credit unions typically charge fewer or lower fees on accounts. They often refund ATM fees and participate in shared networks, giving members access to over 30,000 free ATMs nationwide. Banks tend to have higher maintenance and transaction fees, which can add up over time. Additionally, credit unions return over $37 billion annually in financial benefits through lower fees and better rates, contributing to substantial savings for members. Their community focus and personalized service further enhance their appeal. Leadership and staff often have closer ties to local residents, fostering trust and satisfaction. While banks may offer more branches and faster adoption of new technology, credit unions have narrowed this gap with features like mobile deposits, online bill pay, and shared branching access, providing convenience without sacrificing community-oriented service.

Frequently Asked Questions

How Do Interest Rates Differ Between Credit Unions and Banks?

You’ll often find that credit unions offer higher interest rates on savings and lower rates on loans compared to banks. Because credit unions are non-profit, they pass the savings onto members in the form of better rates. Banks, aiming for profit, might have slightly lower interest rates for savers but tend to charge higher interest on loans. Your choice depends on whether you prioritize earning more or paying less.

Are Credit Unions Safer Than Banks During Financial Crises?

You’re probably wondering if credit unions are safer than banks during financial crises. The truth is, credit unions are like tiny, fearless warriors defending your money with a shield of member-owned loyalty. While banks might seem bigger and more intimidating, credit unions are often more stable because they’re nonprofit, focus on members, and have strong community ties. So, yes, during tough times, they can be just as safe—sometimes even safer!

Can I Use Credit Union Services Nationwide?

Yes, you can use credit union services nationwide, but it depends on the credit union’s network. Many credit unions participate in shared branching and ATM networks, giving you access across the country. You’ll want to check if your credit union offers these services. Keep in mind, not all credit unions are part of extensive networks, so your access might be limited compared to a bank with widespread branches and ATMs.

What Are the Membership Eligibility Requirements for Credit Unions?

You can usually join a credit union if you meet specific eligibility criteria, which often include living, working, or worshiping in a particular area or belonging to a certain organization or employer. Some credit unions also have membership through family or community ties. You’ll need to provide proof of eligibility, such as ID or employment details, to open an account. The requirements vary, so check with each credit union for their specific rules.

How Do Fees Compare Between Credit Unions and Traditional Banks?

You’ll generally find that credit unions charge lower fees than traditional banks. They often have minimal or no monthly maintenance fees, and their overdraft and ATM fees tend to be more affordable. Banks, on the other hand, may impose higher fees for account maintenance, ATM usage, and overdrafts. By choosing a credit union, you can save money on fees, making it a cost-effective option for managing your finances.

Conclusion

So, now that you see the differences between credit unions and banks, which option feels like the right fit for you? Whether you value personalized service and better rates or prefer the convenience of extensive branches and advanced technology, the choice depends on your financial needs. Remember, understanding your priorities helps you make smarter decisions. After all, isn’t your financial future worth choosing the institution that aligns best with your goals?