To decode your paycheck, start by understanding that several deductions lower your gross pay to your net amount. These include taxes like federal, state, and local income taxes, along with FICA taxes for Social Security and Medicare. Benefits such as health insurance and retirement contributions are also deducted, along with any court-ordered garnishments. Knowing how each deduction affects your take-home pay helps you plan better—if you want to explore more details, keep going.

Key Takeaways

- Deductions include taxes, FICA, benefits, court-ordered garnishments, and voluntary contributions, which all reduce gross pay to net pay.

- Federal withholding depends on your W-4 allowances; more allowances mean less tax withheld.

- Benefits deductions like health insurance and retirement plans can lower current taxable income and support future needs.

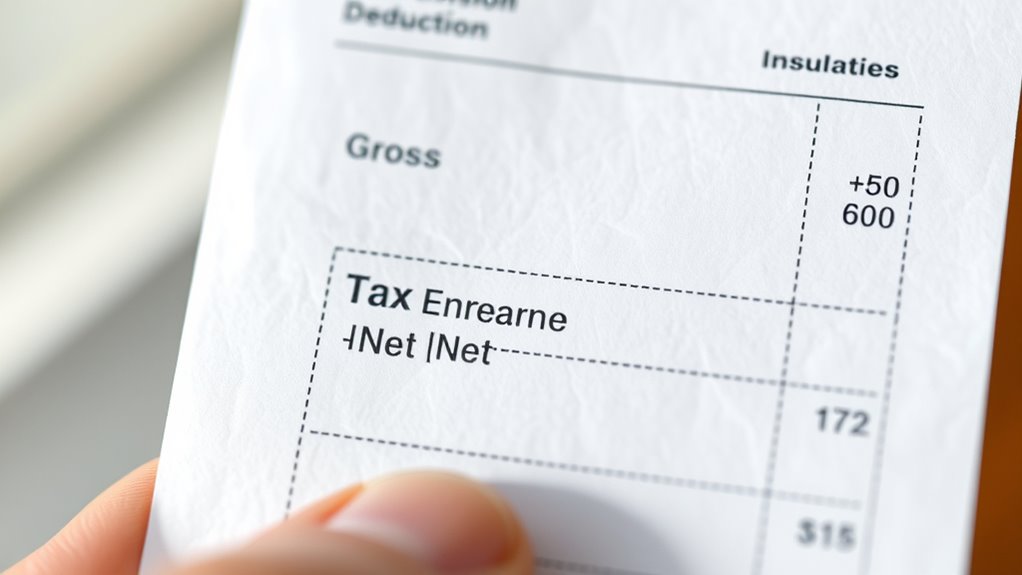

- Your paycheck stub shows gross earnings and itemized deductions, helping you understand your net pay.

- Properly understanding deductions helps you plan finances and make informed decisions about savings and spending.

Have you ever wondered what all the numbers on your paycheck really mean? When you look at your pay stub, it can seem overwhelming with all those lines and figures. But understanding the deductions section is key to knowing how much money you actually take home. Deductions are amounts subtracted from your gross pay, and they serve different purposes — from taxes to benefits and other obligations. Knowing what these deductions are and why they’re there helps you manage your finances better.

First, taxes are the biggest chunk of deductions. Federal income taxes are withheld based on the information you provided on your W-4 form. The more allowances you claim, the less is taken out; fewer allowances mean more taxes are withheld. State and local taxes may also be deducted, depending on where you work and live. These taxes fund public services, infrastructure, and government programs. Alongside these, FICA taxes—comprising Social Security and Medicare—are automatically deducted. Social Security takes 6.2% of your gross income up to a yearly cap, while Medicare is 1.45%, with an extra 0.9% for higher earners. These deductions guarantee you’ll receive benefits when you retire or need healthcare coverage in the future. Although these taxes reduce your current paycheck, they contribute to your security later on.

Benefits are another common deduction, often including health insurance premiums or retirement contributions. If your employer offers health insurance, part of your premium may be deducted directly from your paycheck. Retirement savings plans like a 401(k) are also voluntary deductions, which help you build savings for retirement while reducing your taxable income now. Some deductions are court-ordered, like garnishments, which are taken from your wages for unpaid debts or legal obligations. Others, like voluntary contributions, give you control over your savings and benefits, helping you plan for the future without needing to make separate payments. Understanding these deductions can also help you identify areas where you might optimize your financial planning.

While these deductions are necessary and often beneficial, it’s good to understand how they impact your net pay—the amount you actually receive. Your net pay is your gross pay minus all deductions and taxes. It’s the money you can spend, save, or invest. Pay stubs usually display year-to-date figures, showing how much you’ve earned and paid in deductions over the year, giving you a broader view of your financial picture. By understanding these deductions, you get a clearer picture of your paycheck’s composition and can make smarter financial decisions. Ultimately, knowing what’s deducted and why helps you plan better, ensuring you’re prepared for future expenses and long-term goals.

Top picks for "understand paycheck decod"

Open Amazon search results for this keyword.

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

How Are My Deductions Calculated?

Your deductions are calculated based on your gross paycheck, with percentages or fixed amounts applied according to your earnings and applicable laws. For taxes, your employer uses your W-4 form to determine withholding amounts. Other deductions, like health insurance or retirement contributions, are often a set percentage or fixed amount. Your paycheck stub shows these calculations clearly, so you can see how much is taken out and why.

Can I Opt Out of Any Deductions?

Yes, you can usually opt out of certain deductions, like voluntary retirement contributions or charitable donations. Check with your HR or payroll department to see what’s available and what procedures you need to follow. Keep in mind, some deductions, such as taxes or Social Security, are mandatory and can’t be eliminated. Always review your pay stub and ask questions if you’re unsure about any deductions.

Why Did My Deductions Change This Month?

When your deductions change unexpectedly, it’s often a sign that something shifted on your payroll. Maybe your health insurance premium increased, or your retirement contributions adjusted due to new plan options. It’s worth checking your recent pay stub or speaking with HR to get to the bottom of it. Don’t assume it’s a mistake—sometimes, the devil is in the details, and staying informed helps you avoid surprises down the road.

Are Deductions Different for Part-Time Workers?

Yes, deductions can be different for part-time workers. Since your hours and earnings are usually lower, your tax withholdings, Social Security, and Medicare contributions may be adjusted accordingly. Employers often base deductions on your income level, so part-time employees might see smaller amounts deducted compared to full-time workers. Keep in mind, some benefits or retirement contributions might also vary based on your work hours and employment status.

How Do Deductions Affect My Net Pay?

Imagine you earn $1,000 weekly, and $200 is deducted for taxes and insurance. These deductions lower your gross pay, leaving you with a net pay of $800. Deductions directly reduce your take-home pay, so understanding them helps you budget better. Any increase in deductions, like higher taxes or insurance premiums, will decrease your net pay, affecting how much money you have for expenses and savings.

Conclusion

Now that you know how your paycheck is broken down, it’s like having a map to navigate your finances. Understanding deductions helps you see where your money goes and makes managing your budget easier. Just like a puzzle, each piece fits together to show the full picture of your earnings. So, take charge of your money with confidence—your paycheck isn’t just a number, it’s a tool to help you reach your goals.