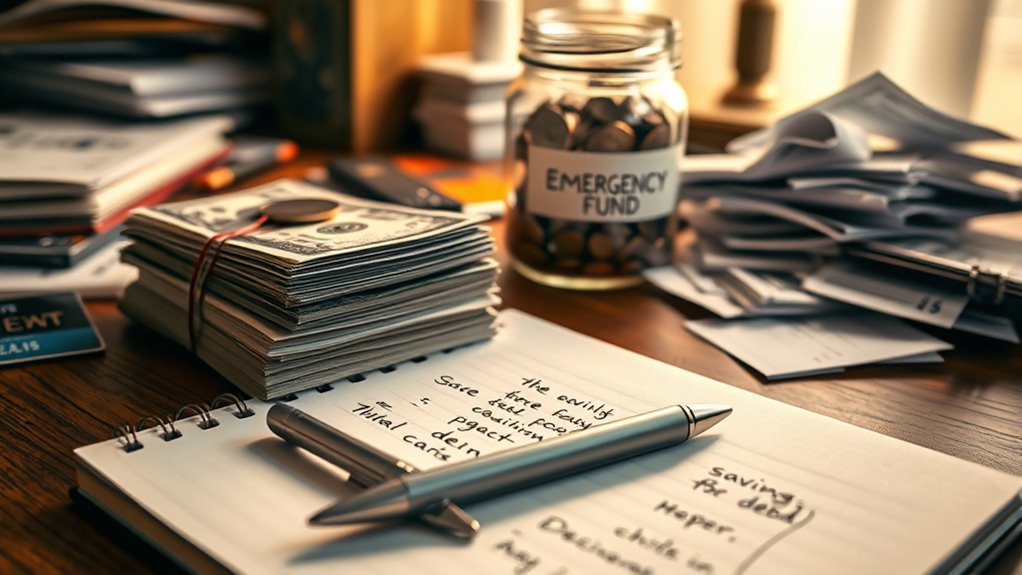

When deciding between building an emergency fund or paying off debt, focus on your biggest financial risks first. If you have high-interest debt, paying it down can save you money long-term, but having even a small emergency fund (around $1,000) provides vital protection. Ideally, balance both goals, especially if your debt carries low interest. Priorities vary based on your situation, so understanding when to focus on each can help secure your financial future. Keep exploring to find what works best for you.

Key Takeaways

- Building an emergency fund first provides a financial safety net, reducing reliance on high-interest debt during crises.

- Prioritize paying off high-interest debt to save money on interest and improve cash flow over time.

- Simultaneously saving a small emergency fund while tackling debt can balance immediate security and debt reduction.

- Focus on emergency savings if debt is manageable but there’s no safety net for unexpected expenses.

- Address both strategies gradually, starting with small savings and high-interest debt, to optimize financial stability.

Deciding whether to focus on building an emergency fund or paying down debt is a common dilemma for many Americans. You’re likely wondering which should take priority to secure your financial future. The truth is, both are essential, but the order of focus depends on your current situation. Right now, many Americans are in a precarious spot—36% have more credit card debt than emergency savings, and 24% have no savings at all. That means a significant portion of your neighbors are vulnerable to unexpected expenses, job loss, or emergencies. Without a safety net, even a small surprise, like a $400 medical bill or car repair, can derail your finances, forcing you to rely on high-interest credit or loans. Nearly 70% of people worry about covering a month’s expenses if their income suddenly stopped, highlighting how fragile many are without sufficient savings.

Many Americans are vulnerable without enough savings, risking financial setbacks from unexpected expenses.

On the other hand, carrying debt, especially high-interest credit card debt, can quickly spiral out of control. Credit card rates often exceed 15% annually, which means your debt grows faster than most savings accounts can earn interest. If you’re juggling debt without savings, you risk falling behind on payments, damaging your credit score, and paying more in interest over time. Data shows that 40% of consumers with no emergency savings have debts more than 60 days past due, compared to just 19% with some savings. This illustrates that the absence of an emergency fund makes you more vulnerable to financial setbacks, especially when unexpected costs arise. Meanwhile, only about half of US adults have three months’ worth of expenses saved—an amount experts recommend for financial security—so many are still unprepared for worst-case scenarios. In fact, having an emergency fund can prevent small setbacks from turning into major financial crises.

Experts generally advise saving three to six months of living expenses in an emergency fund, but it’s also fundamental to address high-interest debt first. Building even a small emergency fund can dramatically reduce reliance on credit during crises, but ignoring high-interest debt can be costly. Paying off debt, especially the most expensive, can save you hundreds or thousands in interest, freeing up cash flow in the long run. Many people find balancing both strategies effective—paying minimums on all debts while funneling extra money into the highest-interest ones, or using the snowball method to gain momentum by tackling smaller debts first. Ultimately, the best approach depends on your financial priorities and circumstances. If your debt is overwhelming, focusing on paying it down first could lower your overall costs. But if you’re completely unprotected against emergencies, building even a modest savings cushion should come first.

BLUETTI Elite 30 V2 Portable Power Station 600W (Power Lifting 1500W), 288Wh LiFePO4 Battery with 10ms UPS, Emergency Backup Power for Home Blackout/Winter Storm, Solar Generator for Camping/Road Trip

[288Wh On-the-Go Power] - Only 9.4 lbs lightweight, carry it anywhere during storms! 288Wh capacity meets daily &...

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

How Much Should I Aim to Save for My Emergency Fund?

You should aim to save at least three to six months’ worth of living expenses for your emergency fund. Start by calculating your essential costs, like rent, utilities, groceries, and insurance. Then, set a monthly savings goal to reach that amount gradually. Having this cushion guarantees you’re protected against unexpected expenses or income disruptions, giving you peace of mind and financial stability in tough times.

Is It Better to Pay off High-Interest Debt First?

They say, “Don’t put all your eggs in one basket,” and that applies here. It’s smarter to pay off high-interest debt first because the interest costs add up fast, eating into your finances. Clearing high-interest debt saves you money long-term and improves your credit score. Once that’s under control, you can focus on building your emergency fund. Prioritizing this way makes your financial foundation stronger and more secure.

Can I Have Both an Emergency Fund and Debt Payoff Simultaneously?

Yes, you can have both an emergency fund and pay off debt at the same time. Start by building a small emergency fund of about $500 to $1,000 to cover unexpected expenses. Then, allocate extra money toward debt repayment while maintaining regular savings. This balanced approach helps protect you from emergencies and reduces your debt faster, giving you financial security and peace of mind.

What Qualifies as an Emergency Expense?

Think of an emergency expense as a surprise thunderstorm—unexpected and urgent. It includes medical bills, car repairs, or sudden job loss costs. These are expenses you can’t plan for and must cover quickly to avoid financial drowning. For example, when your car breaks down unexpectedly, having an emergency fund helps you stay afloat. Generally, aim to save enough to cover three to six months of essential expenses for true emergencies.

How Long Does It Typically Take to Build an Emergency Fund?

It usually takes between three to six months of living expenses to build a solid emergency fund. The timeline depends on your income, expenses, and savings rate. You can speed up the process by setting aside a fixed amount each month and cutting unnecessary costs. Stay consistent and focused, and you’ll gradually accumulate enough to cover unexpected emergencies, giving you peace of mind and financial security.

Portable Solar Generator, 300W Portable Power Station with Foldable 60W Solar Panel,110V Pure Sine Wave 280Wh Battery Power Pack with USB DC AC Outlet for Camping Smart Devices RV Van Outdoor-Orange

Portable Generator with 60W Solar Panel Included: with a big battery pack, ZeroKor 300W power stations Generator are...

As an affiliate, we earn on qualifying purchases.

Conclusion

Think of your financial journey like steering a ship through calm and stormy seas. Building an emergency fund is like securing your lifeboat, ready for sudden storms, while paying off debt is steering your ship toward calmer waters. Ideally, you want both, but if you must choose, prioritize creating that safety net first. That way, when rough waters come, you’ll be anchored securely, and your voyage can continue smoothly toward financial stability.

SOLUPUP Portable Power Station 90,000mAh, 288Wh LiFePO4 Battery Bank, 300W (Peak 600W) Solar Generator, with 110V AC Outlet for Camping & Emergency Backup

【Power Up Everything Anywhere】: This ultra-portable power station packs a massive 288Wh LiFePO4 battery (90,000mAh) delivering 300W pure...

As an affiliate, we earn on qualifying purchases.

MARBERO Portable Power Station 88Wh Camping Lithium Battery Solar Generator Fast Charging with AC Outlet 120W Peak Power Bank(Solar Panel Optional) for Home Backup Outdoor Emergency RV Van Hunting

EFFICIENT CHARGING: Use the adapter included in the package to charge the power station from 0 to 80%...

As an affiliate, we earn on qualifying purchases.